41 yield of zero coupon bond

How do I Calculate Zero Coupon Bond Yield? (with picture) The zero coupon bond yield is easier to calculate because there are fewer components in the present value equation. It is given by Price = (Face value)/ (1 + y) n, where n is the number of periods before the bond matures. This means that you can solve the equation directly instead of using guess and check. calculator.me › savings › zero-coupon-bondsZero Coupon Bond Value Calculator: Calculate Price, Yield to ... Calculating Yield to Maturity on a Zero-coupon Bond. YTM = (M/P) 1/n - 1. variable definitions: YTM = yield to maturity, as a decimal (multiply it by 100 to convert it to percent) M = maturity value; P = price; n = years until maturity; Advantages of Zero-coupon Bonds. Most bonds typically pay out a coupon every six months.

US Treasury Zero-Coupon Yield Curve - NASDAQ - Datastore US Treasury Zero-Coupon Yield Curve From the data product: US Federal Reserve Data Releases (60,654 datasets) Refreshed 10 hours ago, on 7 Jul 2022 Frequency daily Description These yield curves...

Yield of zero coupon bond

How to Calculate the Yield of a Zero Coupon Bond Using Forward Rates? Then now we just subtract 1 from each side so that's gonna give us 0.066 is equal to our yield to maturity on a five-year zero-coupon bond and another way of expressing that 0.066 is 6.6% that's the same thing it's just our way of expressing that decimal. en.wikipedia.org › wiki › Current_yieldCurrent yield - Wikipedia a discount: YTM > current yield > coupon yield; a premium: coupon yield > current yield > YTM; par: YTM = current yield = coupon yield. For zero-coupon bonds selling at a discount, the coupon yield and current yield are zero, and the YTM is positive. See also. Adjusted current yield; References Zero Coupon Bond (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest

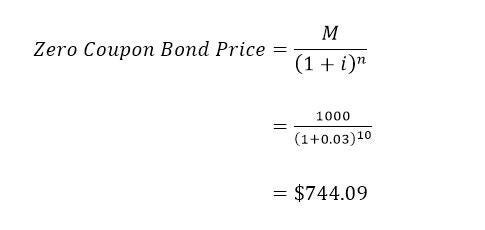

Yield of zero coupon bond. How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816) Zero Coupon Bond Yield Calculator - Find Formula, Example & more The yield of the bond will be. The formula is: Zero Coupon Bond Effective Yield = ( (Face Value of Bond / Present Value of Bond) ^ (1 / Period)) - 1. The process of solution we need to use is: Zero Coupon Bond Effective Yield = ( (1000 / 700) ^ (1 / 5)) - 1. Here, the bond will provide the investor with a yield of 7.39%. Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. That definition assumes a positive time value of money. It does not make periodic interest payments or have so-called coupons, hence the term zero coupon bond. Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

› knowledge › zero-coupon-bondZero-Coupon Bond: Formula and Excel Calculator To calculate the yield-to-maturity (YTM) on a zero-coupon bond, first divide the face value (FV) of the bond by the present value (PV). The result is then raised to the power of one divided by the number of compounding periods. Zero-Coupon Bond YTM Formula. Yield-to-Maturity (YTM) = (FV / PV) ^ (1 / t) – 1; Zero-Coupon Bond Risks Zero Coupon Yield Curve - The Thai Bond Market Association Zero Coupon Yield Curve 0 10 20 30 40 50 60 TTM (yrs.) 0.00 1.00 2.00 3.00 4.00 5.00 6.00 Yield (%) ThaiBMA Zero Coupon Yield Curve as of Tuesday, May 3, 2022 ThaiBMA Government Bond Yield Curve as of 03 May 2022 Export to Excel Remark: 1. Zero Coupon Bond Yield: Formula, Considerations, and Calculation Consider a $1,000 zero-coupon bond that has two years until maturity. The bond is currently valued at $925, the price at which it could be purchased today. The formula would look as follows: = (1000/925)^ (1/2)-1. When solved, this equation produces a value of 0.03975, which would be rounded and listed as a yield of 3.98%. Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter Zero-Coupon Bond Yield = F 1/n PV - 1 Here; F represents the Face or Par Value PV represents the Present Value n represents the number of periods I feel it necessary to mention an example here that will make it easy to understand how to calculate the yield of a zero-coupon bond.

Yield Python Bond Curve A cursory look at the dynamics of zero coupon bond yield curves Which is more volatile, a 20-year zero coupon bond or a 20-year 4 105 with a delta of 0 The yield curve is simply the yields on bonds of varying maturities, typically from three months to 30 years, plotted on a graph One way to price a bond is based on individual investor's ... Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ So a 10 year zero coupon bond paying 10% interest with a $1000 face value would cost you $385.54 today. In the opposite direction, you can compute the yield to maturity of a zero coupon bond with a regular YTM calculator. Zero Coupon Bonds India- Invest in Zero Coupon Bonds Without any intermittent coupon payments, the calculation of yield to maturity of a zero coupon bond is as follows: (Face value/ current market price)*(1/years to maturity) - 1 . Advantages of Zero Coupon Bonds . Investors often compare zero coupon bonds with other fixed income options so as to check in for minimal risks. The returns on zero ... Zero-Coupon Bond Yield - Harbourfront Technologies A zero-coupon bond with a face value of $1,000 has five years to maturity. The current price of the bond is $900 in the market. Therefore, the following formula can help in the calculation of the zero-coupon bond yield. Zero-Coupon Bond Yield = [Face Value / P]^1/n - 1. Zero-Coupon Bond Yield = [$1,000 / $900]^ (1/5) - 1.

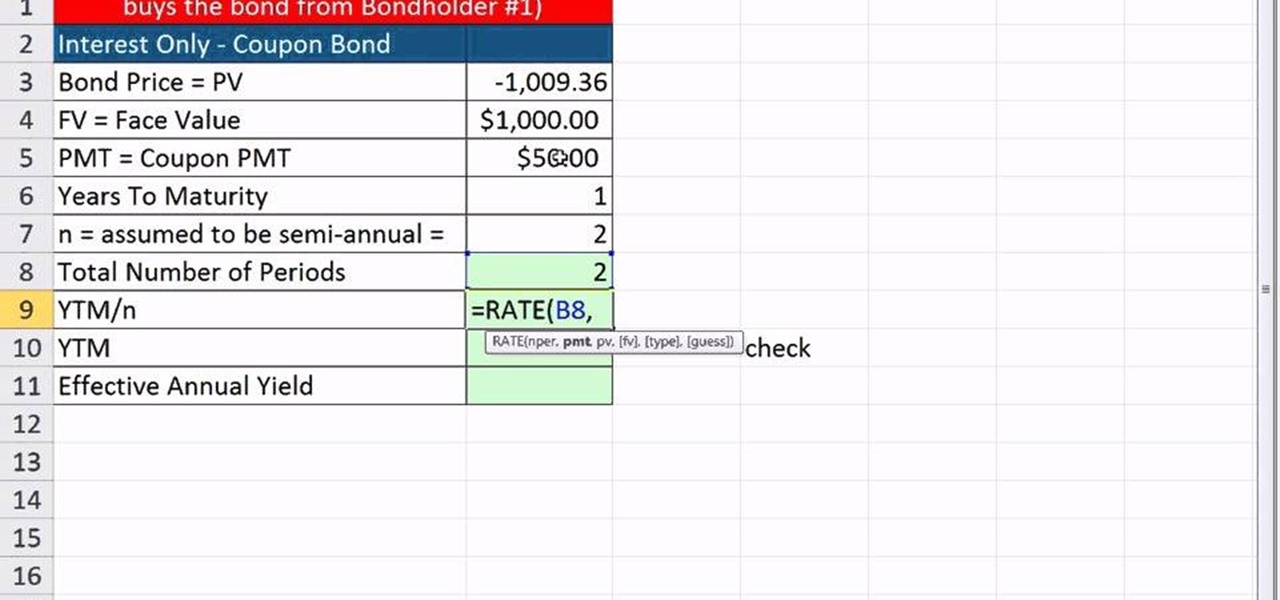

How to Calculate YTM and effective annual yield from bond cash flows in ...

Value and Yield of a Zero-Coupon Bond | Formula & Example The forecasted yield on the bonds as at 31 December 20X3 is 6.8%. Find the value of the zero-coupon bond as at 31 December 2013 and Andrews expected income for the financial year 20X3 from the bonds. Value of Total Holding = 100 × $553.17 = $55,317 Expected accrued income = Value at the end of a period − Value at the start of a period

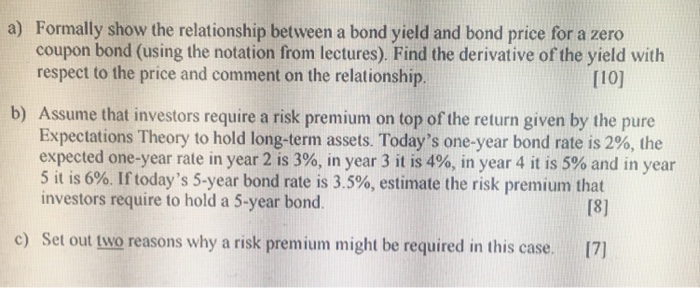

Solved: Formally Show The Relationship Between A Bond Yiel... | Chegg.com

› ask › answersZero Coupon Bond Yield: Formula, Considerations, and Calculation Mar 09, 2022 · Zero-Coupon Bond YTM Example . Consider a $1,000 zero-coupon bond that has two years until maturity. The bond is currently valued at $925, the price at which it could be purchased today. The ...

Bonds ppt

Bond Economics: Primer: Par And Zero Coupon Yield Curves Within a single currency, there are often several yield curves of interest. The relationship between the zero rate and the discount factor is: DF (t) = 1/ (1+r)^t, where DF is the discount factor, and r is the zero rate for maturity t (in years). One of the important properties of the discount factor is that it is equal to 1 at t=0.

Bond Yield Calculator Zero Coupon - CALCULUN

› bootstrapping-yield-curveBootstrapping | How to Construct a Zero Coupon Yield Curve in ... Zero-Coupon Rate for 2 Years = 4.25%. Hence, the zero-coupon discount rate to be used for the 2-year bond will be 4.25%. Conclusion. The bootstrap examples give an insight into how zero rates are calculated for the pricing of bonds and other financial products. One must correctly look at the market conventions for proper calculation of the zero ...

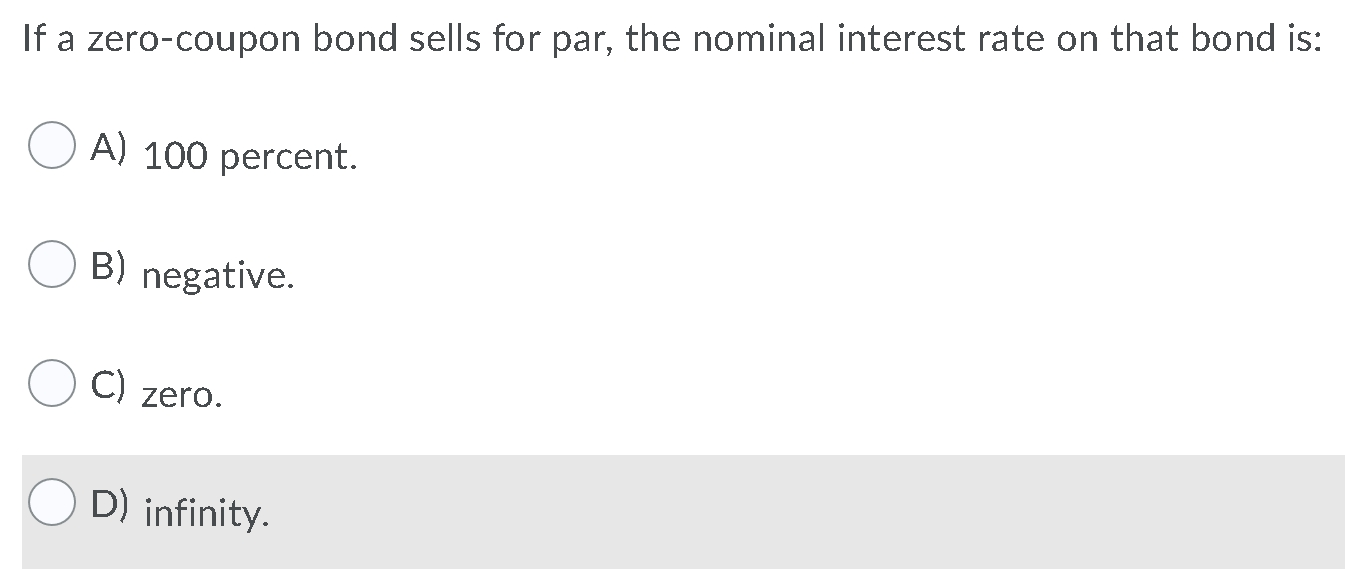

Solved: If A Zero-coupon Bond Sells For Par, The Nominal I... | Chegg.com

What Is a Zero Coupon Yield Curve? (with picture) The zero coupon rate is the return, or yield, on a bond corresponding to a single cash payment at a particular time in the future. This would represent the return on an investment in a zero coupon bond with a particular time to maturity. The zero coupon yield curve shows in graphical form the rates of return on zero coupon bonds with different ...

PPT - Chapter 2 Bond Prices and Yields PowerPoint Presentation, free ...

› terms › zZero-Coupon Bond Definition - Investopedia Nov 11, 2021 · Zero-Coupon Bond: A zero-coupon bond is a debt security that doesn't pay interest (a coupon) but is traded at a deep discount, rendering profit at maturity when the bond is redeemed for its full ...

Bonds part 1

home.treasury.gov › policy-issues › financing-theInterest Rate Statistics | U.S. Department of the Treasury NOTICE: See Developer Notice on February 2022 changes to XML data feeds. Daily Treasury PAR Yield Curve Rates This par yield curve, which relates the par yield on a security to its time to maturity, is based on the closing market bid prices on the most recently auctioned Treasury securities in the over-the-counter market. The par yields are derived from input market prices, which are ...

How did physical bond coupons actually work? - Quora

Yield Curves for Zero-Coupon Bonds - Bank of Canada These files contain daily yields curves for zero-coupon bonds, generated using pricing data for Government of Canada bonds and treasury bills. Each row is a single zero-coupon yield curve, with terms to maturity ranging from 0.25 years (column 1) to 30.00 years (column 120). The data are expressed as decimals (e.g. 0.0500 = 5.00% yield).

What is a Zero-Coupon Bond? Definition, Features, Advantages ...

14.3 Accounting for Zero-Coupon Bonds - Financial Accounting Explain how interest is earned on a zero-coupon bond. Understand the method of arriving at an effective interest rate for a bond. Calculate the price of a zero-coupon bond and list the variables that affect this computation. Prepare journal entries for a zero-coupon bond using the effective rate method. Explain the term "compounding."

Fixed Income: Spot Rate Calculation – Forward Rate Calculation ...

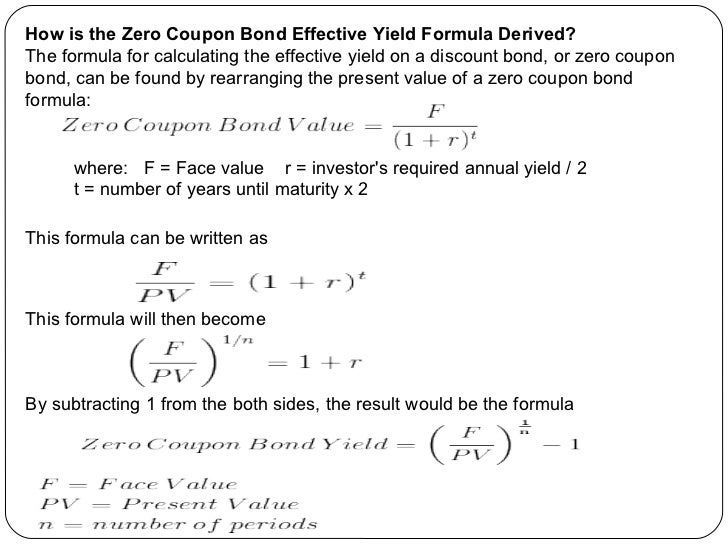

Zero Coupon Bond Yield - Formula (with Calculator) The formula for calculating the effective yield on a discount bond, or zero coupon bond, can be found by rearranging the present value of a zero coupon bond formula: This formula can be written as This formula will then become By subtracting 1 from the both sides, the result would be the formula shown at the top of the page. Return to Top

Zero coupon bond yield to maturity calculator 778066-Coupon bond yield ...

Zero Coupon Bond Value - Formula (with Calculator) A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

6.3 The Zero Coupon Bond Case

Advantages and Risks of Zero Coupon Treasury Bonds If a zero-coupon bond is purchased for $1,000 and given away as a gift, the gift giver will have used only $1,000 of their yearly gift tax exclusion. The recipient, on the other hand, will receive...

Zero Coupon Bond | Bonds (Finance) | Yield (Finance)

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

Advanced Bond Concepts: Bond Pricing | Investopedia

Zero Coupon Bond (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest

Bond pricing - Bogleheads

en.wikipedia.org › wiki › Current_yieldCurrent yield - Wikipedia a discount: YTM > current yield > coupon yield; a premium: coupon yield > current yield > YTM; par: YTM = current yield = coupon yield. For zero-coupon bonds selling at a discount, the coupon yield and current yield are zero, and the YTM is positive. See also. Adjusted current yield; References

Zero Coupon Bond Study | Bonds (Finance) | Yield Curve

How to Calculate the Yield of a Zero Coupon Bond Using Forward Rates? Then now we just subtract 1 from each side so that's gonna give us 0.066 is equal to our yield to maturity on a five-year zero-coupon bond and another way of expressing that 0.066 is 6.6% that's the same thing it's just our way of expressing that decimal.

Bond Discounting I Types I Examples I Formula I Bonds Valuation

Post a Comment for "41 yield of zero coupon bond"