39 duration for zero coupon bond

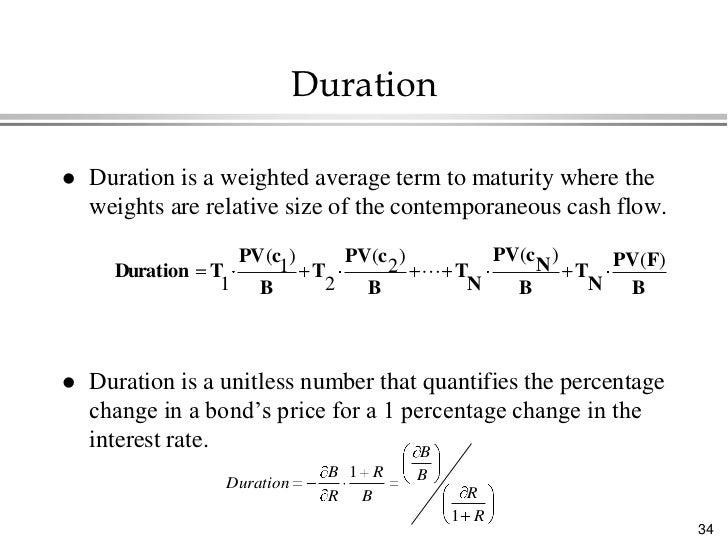

The duration of a zero coupon bond is equal to the ... The duration of a zero-coupon bond is equal to the maturity of that bond. For example, suppose we have a zero-coupon bond with 2 years to maturity trading at a YTM of 25%. If you calculate the duration you will find that it will be equal to two years. 3.7.4. Duration of an irredeemable bond. An irredeemable bond is a perpetuity. Macaulay Duration - Overview, How To Calculate, Factors A zero-coupon bond assumes the highest Macaulay duration compared with coupon bonds, assuming other features are the same. It is equal to the maturity for a zero-coupon bond and is less than the maturity for coupon bonds. Macaulay duration also demonstrates an inverse relationship with yield to maturity.

Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

Duration for zero coupon bond

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond . Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield. What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount ...12 answers · 16 votes: The duration of a zero coupon bond is the number of years to maturity What is the duration of a 10 year zero coupon bond.docx ... What is the duration of a 10 year zero coupon bond? A long-term discount bond with ten years to maturity, a so-called zero-coupon bond, makes all of its payments at the end of the ten years, whereas a 10% coupon bond with ten years to maturity makes substantial cash pay- ments before the maturity date.

Duration for zero coupon bond. What is the duration of a zero coupon bond? - Quora Originally Answered: what is the duration of a zero coupon bond? Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. Modified Duration - Zero Coupon Bond Modified Duration ... We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%. Duration - NYU Stern Debt Instruments and Markets. Professor Carpenter. Duration. 4. •For zero-coupon bonds, there is a simple formula relating the zero price to the zero rate.17 pages Zero-coupon bond - Wikipedia Zero coupon bonds may be long or short-term investments. Long-term zero coupon maturity dates typically start at ten to fifteen years. The bonds can be held until maturity or sold on secondary bond markets. Short-term zero coupon bonds generally have maturities of less than one year and are called bills.

duration of zero coupon bonds | Forum | Bionic Turtle With respect to a zero coupon bond, Macaulay duration = maturity, and therefore must be a monotonically increasing function of maturity. On the other hand, DV01 of a zero (or deeply discounted) is not strictly increasing as DV01 = P*D/10,000 and the numerator has offsetting effects. If you'd kindly reference, I can fix? Thanks! Apr 7, 2012 #3 S Zero Coupon Bond Calculator - MiniWebtool The Zero Coupon Bond Calculator is used to calculate the zero-coupon bond value. Zero Coupon Bond Definition. A zero-coupon bond is a bond bought at a price lower than its face value, with the face value repaid at the time of maturity. It does not make periodic interest payments. When the bond reaches maturity, its investor receives its face value. Macaulay's Duration | Formula | Example Duration of Bond A is 4.5, i.e. the maturity period (in years) of the zero-coupon bond. Duration of Bond B is calculated by first finding the present value of each of the annual coupons and maturity value. Annual coupon is $50 (i.e. 5% of the $1,000) and the maturity value is $1,000. 2022 CFA Level I Exam: CFA Study Preparation - AnalystNotes Bond duration is affected by many variables. The fraction of the period that has gone by (t/T). A plot of Macaulay duration (or modified duration) against time for a single bond with constant yield will show a saw-tooth pattern, with Macaulay duration declining steadily until a coupon payment results in an upwards jump.. The Macaulay duration of a zero-coupon bond is its time-to-maturity.

fixed income - Duration of callable zero coupon bond ... A 10-year zero coupon bond is callable annually at par (its face value) starting at the beginning of year 6. Assume a flat yield curve of 10%. What is the bond duration? A- 10 Years B- 5 Years C- 7.5 Years D- Cannot be determined based on the data given. According to me it should be 10 years as the duration of a zero coupon bond is always equal ... Zero Duration ETF List - ETFdb.com Zero Duration and all other bond durations are ranked based on their aggregate 3-month fund flows for all U.S.-listed bond ETFs that are classified by ETF Database as being mostly exposed to those respective bond durations. 3-month fund flows is a metric that can be used to gauge the perceived popularity amongst investors of Zero Duration ... Macaulay Duration Zero Coupon Bond - RAEE Other factors include coupon rate and frequency, bond yield and any call features written into the bond. Like maturity, duration is also expressed in years. Note that any bond with a non-zero coupon will have a duration shorter than its maturity. For example, a 30 year bond with a 7% coupon and a 6% YTM has a duration of only 14.2 years ... Zero-Coupon Bond Definition - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

Bond valuation

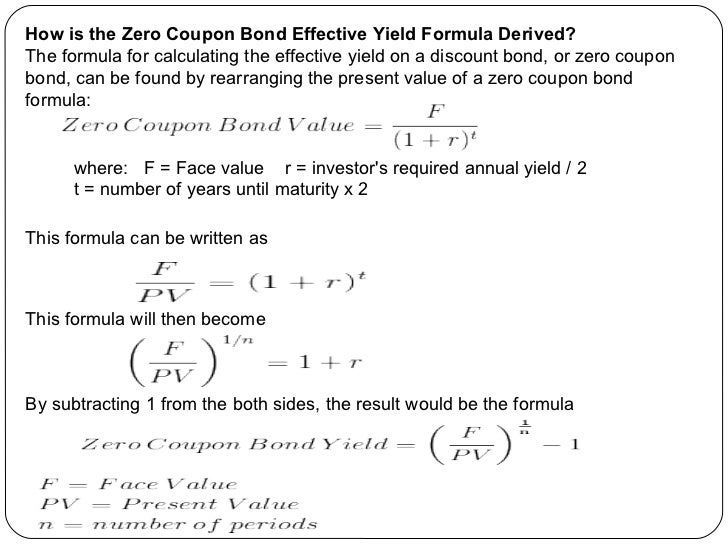

The Macaulay Duration of a Zero-Coupon Bond in Excel ... To compensate for the lack of coupon payment, a zero-coupon bond typically trades at a discount, enabling traders and investors to profit at its maturity date, when the bond is redeemed at its face value. The Formula For Macaulay Duration Macaulay Duration = ∑ i n t i × P V i V where: t i = The time until the i th cash flow from the asset will be

Floating Rate Notes (FRNs) Valuation | Floating Rate Bonds Pricing | FinPricing

Zero Coupon Bond Value Calculator: Calculate Price, Yield ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months.

PPT - Financial Risk Management PowerPoint Presentation, free download - ID:3004009

Zero Coupon Bond (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

3. How to calculate a zero coupon bond, coupon bond prices with Program R - YouTube

Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

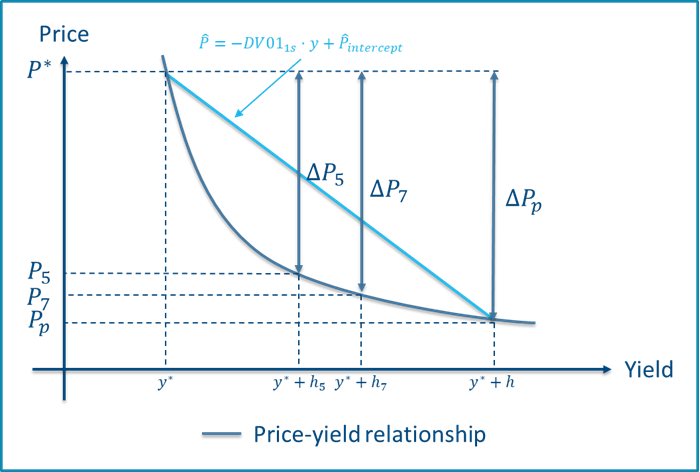

When do key rate measures add up? - Scanrate

Solved What is the approximate duration of a 5-year ... What is the approximate duration of a 5-year zero-coupon bond? O 5 years O 2 years O 3 years 4 years ; Question: What is the approximate duration of a 5-year zero-coupon bond? O 5 years O 2 years O 3 years 4 years . This problem has been solved! See the answer See the answer See the answer done loading.

ZERO COUPON BOND CALCULATOR - BOND CALCULATOR - AIR MILE CALCULATOR

PDF APPENDIX 3A: Duration and Immunization maturity and duration zero-coupon bond or a coupon bond with a five-year duration, the FI would produce a $1,469 cash flow in five years, no matter what happens to interest rates in the immediate future. Next we consider the two strategies: buying five-year deep-discount bonds and buying five-year duration coupon bonds.

Bonds ppt

What Is Duration of a Bond? - TheStreet Definition - TheStreet The easiest duration to calculate is that of a zero-coupon bond. This bond has zero yield, which means it does not pay any interest. Its duration is equal to its time to maturity. When a coupon is...

Zero Coupon Bond - YouTube

What is the duration of a bond? and How to Calculate It ... Duration of a Bond. The duration of a bond does not represent the duration for which an investor holds a bond. Instead, it refers to the relationship between the price of a bond and interest rates of the bond after considering its different characteristics such as yield, coupon rate, maturity, etc.

PPT - Chapter 7 The Valuation and Characteristics of Bonds PowerPoint Presentation - ID:6551199

The Macaulay Duration of a Zero-Coupon Bond in Excel Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and...

united states - Can zero-coupon bonds go down in price? - Personal Finance & Money Stack Exchange

Bond Duration Calculator - Macaulay and Modified Duration ... Formula for Macaulay Duration The Macaulay duration formula (written as a series) is: \frac { 1*\frac {Payment_1} { (1+yield)^1} + 2*\frac {Payment_2} { (1+yield)^2} +...+ (n-1)*\frac {Payment_ {n-1}} { (1+yield)^ {n-1}} + n*\frac {Payment_n+Par\ Value} { (1+yield)^n} } {Current\ Price} C urrent P rice1 ∗ (1+yield)1P ayment1

Bond’s Maturity, Coupon, and Yield Level | CFA Level 1 - AnalystPrep

Solved Which statement is incorrect? Statement 1 ... - Chegg Statement 1: The duration of a zero-coupon bond is the same as its maturity. Statement 2: The longer a bond's duration, the greater its volatility. Statement 3: The duration of any bond is the same as its maturity. Group of answer choices Statement 3 Statement 1 None Statement 2

The Allure Of Zero Coupon Municipal Bonds: A Low Risk Investment With Stable Interest

PDF Duration - New York University Duration 7 For zero-coupon bonds, there is an explicit formula relating the zero price to the zero rate. We use this price-rate formula to get a formula for dollar duration. Of course, with a zero, the ability to approximate price change is not so important, because it's easy to do the exact calculation.

Modified duration of zero-coupond bond (FRM practice question) - YouTube

What is the duration of a 10 year zero coupon bond.docx ... What is the duration of a 10 year zero coupon bond? A long-term discount bond with ten years to maturity, a so-called zero-coupon bond, makes all of its payments at the end of the ten years, whereas a 10% coupon bond with ten years to maturity makes substantial cash pay- ments before the maturity date.

Solved: Prices of zero-coupon bonds reveal the following patter... | Chegg.com

What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount ...12 answers · 16 votes: The duration of a zero coupon bond is the number of years to maturity

Finding YTM of a Zero Coupon Bond (6.2.1) - YouTube

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond . Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

Post a Comment for "39 duration for zero coupon bond"